1

Introduction

2

Context

3

South West Overview

4

Transformative Opportunities

5

Positioning the South West

6

Contact & Feedback

Full Website Menu

Open Navigation

Close Navigation

Competitive advantage tends to come at the intersection of comparative advantage, good market access and opportunity. The South West’s sub-regions feature aspects of different industry sectors although each has focus points based on inherent advantage – resources, agriculture and natural beauty.

The importance of the mining sector to Western Australia is widely acknowledged, but the mining/manufacturing value to the South West is less well recognised. Mining and manufacturing’s value is a third of the total economy and that is growing.

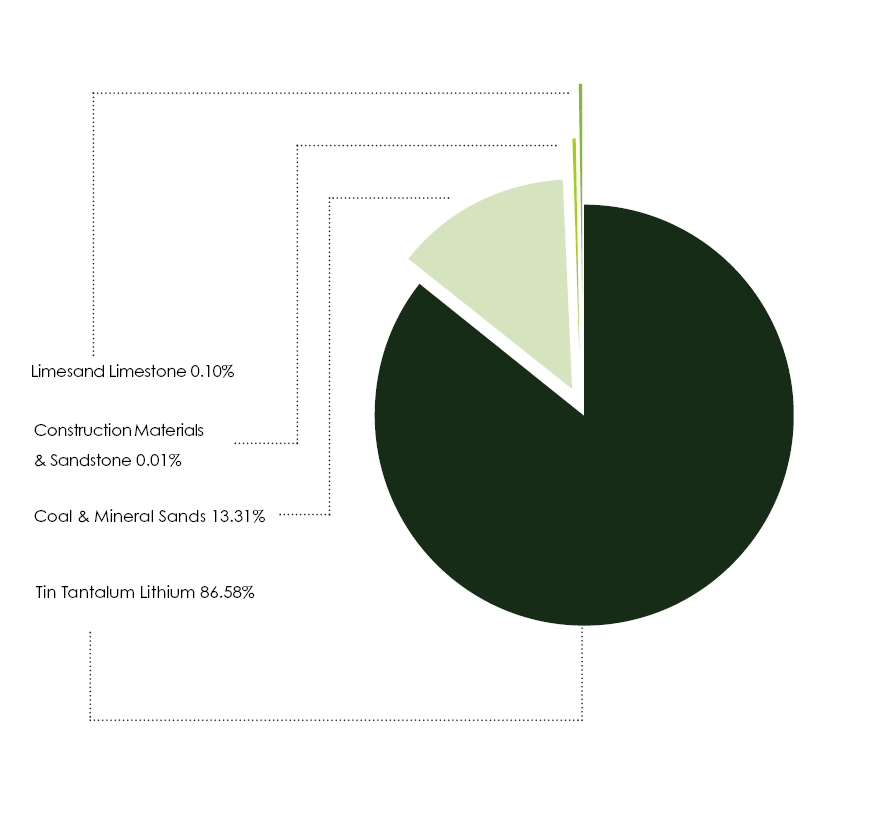

The region is well placed for the future in alumina/bauxite processing, and particularly in lithium-rich spodumene production. The Talison Lithium plant in Greenbushes is in the middle of a 10-year transition. Five years ago output was at 650,000t and last year it was 1.35mt with quarterly sales exceeding $2bn. By 2027 the forecast output is 2.2mt. With an anticipated mine life of more than 20 years, the Kemerton-based lithium processor, Albermarle is also expanding to meet worldwide demand.

In respect of titanium dioxide, compound annual growth rates of 5.3% are predicted through to 2032. The region’s mineral sands enterprises (Iluka and Tronox) contributed almost $900m in sales (2022).

The sectoral picture for employment is muddied since the South West is home to a significant FIFO workforce and Alcoa’s major alumina plant at Waaerup is located just inside the neighbouring Peel region but the bulk of the workforce hails from the South West with exports going through the Port of Bunbury. Mining in the South West employs more than 3,000 persons in-region, while almost that number travel outside the region for work.

Regional METS prospects are outstanding.

Note - Mineral and petroleum sales are necessarily allocated to a single Local Government Area (LGA) and Region, even though mining and processing operations may be located within multiple LGAs and Regions.Sales are allocated to LGAs and Regions based on where a mineral or petroleum product is originally extracted.

Figure 4 - Value of Mining | Source: DEMIRS 2024 Spatial and regional data file

Agriculture, forestry and fishing is a large, fragmented industry that makes contributes $2.76bn (6.3%) to economic output, with Manjimup the leading area and accounting for more than $550m in annual output (ABS June 2024 Gross State Product).

Farming takes up 7,100km2 of land area in a region that has typically enjoyed reliable rainfall. However, this calendar year has been one of the lowest rainfall years in recent memory and producers in the region have struggled with livestock management and survival of plantation trees and vines. Re-examining water needs and how to meet them will be critical as efforts to support adaptation and dry season business management pivots from other areas of the state to the South West.

Being home to smaller farms and more intensive production methods than other primary production regions of the state, the South West faces challenges in the management of chemicals, fertilisers and effluent in areas that are closer to water sources and more urban environments. Scale also impacts on investment in mechanisation/technology upgrades which can reduce labour needs, an issue that has blighted the region especially at harvest time.

The future relocation of Boyanup Saleyards creates an opportunity for developing an agricultural precinct. This would be an enabler for collectively working at scale, value adding and manufacturing products to reduce waste. An agriculture precinct would also play to the region’s strengths given that industry classifications with more than half the State’s total contribution include: onions (100%), avocado (89%), potatoes (86%), apples (84%), dairy production (82%), carrots (53%), and wine grapes (65%).

Image by Frances Andrijich, Newy’s Vegie Patch, Kirup

Figure 5 - Value of agricultural production – South West 21-22 | Source: ABS 2021-22 National Input Output Tables

The value of wine grapes is just over $50m and the value of the wine and spirits industry is collectively $245m (2019). However, the value that the brand brings to Margaret River and the region as a whole is far greater.

Of the South West’s five wine regions, Margaret River leads the way with 100 cellar doors and about 30,000t of grapes harvested contributing 2% of the national crush. Margaret River remains a standout for exports (1.6 million litres, $24m, 2024-25) and leads the nation with 67% of wine sold in the top three price brackets.

The removal of Chinese tariffs saw the Australian export market bounce back and underlined in importance as other markets, particularly North America, have declined (Wine Australia, 2025). Weather conditions have been perfect for viticulture, leading to the 2025 vintage being hailed as exceptional for both red and white varietals and akin to the 2023 standout year.

The Geographe wine region continues to grow in reputation along with The Blackwood Valley, Manjimup and Pemberton regions.

Image by Tourism WA, Fraser Gallop Winery

Fisheries, particularly aquaculture, has increasingly realised its potential particularly in marron farming at Capel and abalone along the south coast. In respect of fishing, the recreational fishing industry has greater value than commercial operations, with almost 18,000 recreational fishers spending more than $305m pa in the South West (Recfishwest 2021).

The timber industry is in the midst of unprecedented change and challenges. Two-thirds of the South West region is native forest but the vast majority of that resource has been set aside for conservation.

South West forestry was traditionally a mix of regrowth native hardwood, plantation hardwood and softwoods. However, commercial harvesting of native forest ended with implementation of the new Forestry Management Plan 2024-2033. This has left WA increasingly reliant on hardwood timber imports, but has created plantation opportunities for softwood (pine) and hardwood (bluegum).

Funded by the Australian Government to 2027-28, the South West Forestry Hub is one of 11 nationally and includes the South West and Great Southern regions. The priorities identified by the South West Timber Hub now focus on supporting growth in plantations and utilisation of forest thinning:

- Undertaking research projects aiming to expand the softwood plantation estate by at least 5,000ha annually, with a focus on integrating commercial trees on farmlands;

- Encouraging full utilisation of the available wood fibre; and

- Ensuring community understanding of the environmental, regional, social and economic benefits from managed forests and woodlands.

Forestry is being challenged by a drying climate. Geographically, the lower south western part of WA enjoys a natural rainfall advantage, although the 600mm precipitation line is retreating (westward). This is impacting on suitable land to establish more plantations.

The onflow from forestry is manufacturing. The Dardanup timber precinct captures Laminex, one of Australia’s leading particle board manufacturers, and Wespine which produces the vast majority of the State’s construction timbers. Koppers produces WA’s power poles. There are other local interests in fibre processing including WAPRES which processes pine and bluegum for both export and domestic sales. Exports were approximately 870k mt (2023).

Timber sourced from sustainable forest management supports a local processing and manufacturing capability. Processing locally grown and harvested timber adds value and jobs while providing our community with the ultimate renewable construction material. However, there is a shortfall of plantation softwood and a need for planting at least an additional 50,000ha to sustain existing processing capacity to meet the forecast industry demand in the years ahead. The State Government committed $350m to plantation softwoods in 2021 but progress has been slow. Considerable opportunities exist for private sector investment in plantations.

New technologies are helping ensure that every fibre of resource is utilised and efficiencies can support opportunities in log peeling, veneer production, and Engineered Wood Products (EWP) including expanding LVL production or alternative cross laminate timber (CLT) manufacturing.

Credit: Planet Ark

While a number of regional communities value tourism, the key industry sector lies in the Capes where tourism jobs (2024) dominate: Busselton 15.2% and Margaret River 17.6%. The sector contributes through FAS but also in retail, services and even manufacturing. ABS metrics note that the FAS category provides 6.1% of all South West jobs. However, the total of tourism jobs for the region is 8.6% compared to tourism employment across Western Australia generally at 5.3%. The economic value of the sector (2024) was estimated at more than $1.7bn with more than half of that in the Capes sub-region: Busselton $666m and Margaret River $325m.

The region clearly benefits from its natural beauty, amazing landscapes and proximity to the Perth intra-state market. Quality events are also strong triggers for regional visitation which is supported by trails, food and beverage, cultural enrichment and visitors seeking positive/wellness experiences.

There are significant opportunities for Aboriginal cultural tourism, building on existing attractions, while new trails, improvements to the existing trails and world class cycling tracks add to the region’s emotional drivers.

Prospects for an increasingly strong sector abound, but the strength of the sector in local employment is also its vulnerability. Given that the South West is noted as the seventh most tourism dependent region in Australia across different measures (Tourism Research Australia), building resilience through capacity and capability building to manage cyclical changes and shocks is essential. The sharing economy has also affected businesses, with Airbnb having an impact on professional accommodation services.

Accommodation and hospitality are traditionally less well paid than other sectors. This can be a challenge when those workers find themselves living in a tourism hotspots where living expenses are typically higher than average. The added complication is the current shortage of affordable housing.

Image by City of Busselton, Boranup Forest

The South West region has a substantial and growing creative economy, with some hotspot areas such as Bunbury, Busselton and Margaret River showing employment levels compara-ble to Perth.

While diverse, creatives lie in these categories:

• Core arts and Cultural industries (e.g. core arts such as literature, music, performing art and visual arts and cultural industries such as film, museums, galleries, photographic studios and libraries

• Creative industries (e.g. sound recording, television and radio, video and computer games, heritage, publishing and print media)

• Wider creative jobs in other industries (e.g. architecture, marketing, advertising, design)

Many creative jobs contribute to the economy but are not located specifically within a creative business. Overall there are 1,467 jobs in the creative sector, but also 1,394 creative jobs that are located in “non-creative” industries. Some examples include computer system and app design across all industries, architectural services in construction, marketing and advertis-ing in almost any business.

Underpinning these ecosystems is the local Capes reputation for quality nationally-recognised events and festivals such as CinéfestOZ which has helped fuel growth of the screen indus-try over the past decade. The Bun-Geo subregion encourage creatives to connect through events such as Bunbury Fringe, the Creative Tech Village hub in Bunbury and also a number of maker spaces being supported by local governments.

Image by City of Bunbury

Changes in consumer behaviour has seen some change and has shaped CBDs in recent years. However, Local Governments have responded and there has been significant investment in Busselton and Eaton.

Nevertheless, online options, cost of living pressures, reduced disposable income and increased commercial rents combine to squeeze retailers.

It has also been recognised that shoppers are likely to demand a more enjoyable experience and greater diversity, so a number of smaller and unique outlets are more appealing than national chains.